We Good, Right? So Why Number Not Go Up?

We Good, Right? So Why Number Not Go Up?

The madness of crowds...

From the moment I first began following bitcoin, I have often been perplexed not only as to the primary mechanism which ultimately influences the bitcoin price but also the best way to model such a mechanism so as to gain a better perspective as to where the market might be headed. Why this incessant fixation on price? Because Bitcoin is, in my opinion, the best available proxy to divine the current and even future state of not merely the global economy but all the many implications and consequences that might unfold with any significant alteration to the trajectory of that economy. At the end of the day as well, I suppose I am a long-term trader looking to increase my bitcoin stack and thus need to be armed with the brushes to be able to paint a general picture of where we are going and possibly when. Only Bitcoin among all the world's investible assets allows non-insiders (i. e. you and me) to reasonably paint such a picture.

Does technical data and raw chart patterns - which are, of course, graphic depictions of the sum total of human activity within a given asset market - give insight into where the price of an asset might be headed, or does fundamental analysis - i. e. news events, press releases, quarterly institutional filings, etc. - primarily drive Bitcoin's value in the eyes of the market? Or is it simply: bitcoin's code ensures that new supply issuance gets cut in half every four years thus if demand stays constant, price (based upon the laws of supply and demand) will naturally trend higher to the point that it begins to gain media attention leading to a speculative frenzy followed quickly by a harsh sell-off and a prolonged accumulation period, all of which is compounded and bolstered by the difficulty adjustment that corrects either up or down depending on the number of bitcoin miners currently securing the network, that adjustment which sets, if not a floor, then at least a firm tether to which bitcoin seldom drops significantly below. Or is it perhaps a combination of all these factors plus "something else"?

Curiously, the more time I spend in this ecosystem, the further I find myself from a sufficient answer. In fact, with each passing day, I am left more bewildered than the day before. I have often tried to explain this "something else" by calling Bitcoin an "entity" which, though it does not have its own will nor is it self-conscious or self-reflective, nevertheless as an idea invested with an incalculable amount of emotional energy, has taken on a "life of its own" and therefore - as any "living" thing - will fight for its own survival. The survivalist tendencies of bitcoin are hard to deny, and it is certainly an intellectual stretch to assume that Bitcoin's indefatigable perseverance is the work of a few dedicated market actors, cypherpunks, coders, "hodlers", rich "whales", and others diligently building and maintaining the bitcoin ecosystem. Though this notion of "Bitcoin the entity" is perhaps a neat and tidy way to tie up many of the loose ends surrounding the mysterious character of this asset, it isn't really helpful when attempting to explain the daily, weekly, and monthly nuances of bitcoin to a newcomer, nor should it necessary inform one's overall investing decisions to a significant degree.

Traditional technical analysis (TA), except in the most general of senses, is a poor method to predict the Bitcoin price, both in the medium and long term, especially if it is exclusively employed. Sure, technical analysis of Bitcoin, primarily because it is unregulated, can be a more reliable way to predict short term price movements than it can with traditional equities, but the nature of Bitcoin's volatile price action always frustrates technical crypto traders by either failing to sufficiently "mean revert" and "back-test previous support" or by blowing away their wildest expectations to the upside or down. Eventually, Bitcoin's tendency to surprise is why so many crypto traders get absolutely wrecked. Though technical analysis is, most assuredly, a craft, the truth is: if anyone could learn it and use it effectively, everyone would do it - and be successful. The reality is, day trading or swing trading or even cycle trading based on technical analysis is extremely difficult, and at best provides traders certain probabilities which, again, Bitcoin is famous for spoiling. Only 5% of day-traders are profitable. Granted, there are dozens of factors that will dictate success and failure in trading, but if technical analysis was as effective as Youtube influencers proclaim it to be, the problem, of course, would not be the TA, but the individual trader. Youtube (as well as other SM platforms I'm guessing, I don't know, I'm not a user) is flush with innumerable "crypto day traders" not because TA is simple or certain, but because they are running a media business that seeks to gain the maximum amount of subscriptions so as to encourage high user engagement on a daily basis. Youtube pays them for this engagement, as do sponsors. There will always be "something" going on in the charts, therefore they have most of their daily content conveniently provided for them, as well as an endless stream of lemmings looking to consume the content so they, too, can get rich off a single trade. This, combined with the fact that these influencers "livestream their multi-million-dollar trades" from their high-rise penthouses in Dubai, makes anyone say, "hey, if that 22-year-old dummy can do it, surely I can." However, how can you verify they are demonstrating their own personal trades and their own penthouses in the first place? And if they're so profitable at trading, why bother with a Youtube channel which, in order to keep up with the daily demand of ravenous content consumers, must be filmed, edited, disseminated, etc? Why not just quietly trade at home? You all know the first rule of Bitcoin: never tell anyone you have any bitcoin - and certainly not how much. Each one of these internet day-traders earns more money selling their "day trading courses" to their large subscription bases than they do from their personal day trading strategies. Again, otherwise why bother?

Rant aside, technical traders don't move markets anyway, they merely seek to capitalize on the moves that are already in the process of unfolding, typically using leverage. What I'm curious about is what precipitates the moves in the first place. Sure, an overleveraged crypto environment can certainly lead to violent price action when Bitcoin gets going, but technicians are incapable of precipitating a move, they merely amplify it. This goes for so-called "whales" too, whom I covered in the last newsletter. Large wallet holders don't tend to initiate market movements but, like leveraged traders, will start to liquidate or accumulate after a move has been confirmed, or until their long-range target has been reached. Because their price floors and liquidation targets, based on the Bitcoin futures market as well as on-chain analysis, tend to flash at similar junctions respective to other large holders, it might appear they act in unison. However, this is far from coordinated activity or outright collusion. Besides, selling a couple billion dollars worth of bitcoin won't move the market much at this point anyway. Most whales have enough money, thus why sell? A Bitcoin whale is a whale because they have long time horizons and tend to trade "spot" (i. e. they don't use leverage but long, short, and trade only what they actually own), or they trade futures, options, covered calls, etcetera. They are not on Coinbase or Bybit monitoring the four-hourly candles from their cell phones. The (very few) billionaires who can be considered individual whales certainly aren't doing this, nor are the major companies and funds that are listed as the biggest wallet addresses on the blockchain. Corporates aren't day trading, they're raising debt to buy Bitcoin for their treasuries. If the actions taken by whales, i. e. a few "anonymous billionaires" (most of whom are in no way anonymous but are, in fact, highly public people like the Winklevoss twins, Tim Draper, and others) actually moved the market, why not simply sell and then place an immediate leveraged short position to further capitalize on the move you just made. They don't because it wouldn't work. Whales have as much "influence" on the Bitcoin price as overleveraged traders, and probably the same amount of trading power in aggregate. They aren't working in unison to crash the market for their benefit; the same goes for "the government" or "insiders" or "wall street". The blockchain enables us to see every transaction in real-time, so there are no secrets, only erroneous assumptions. Maybe I'm getting hung up on the definition of "whale", but I won't be swayed from my belief that their influence is overstated. I'm sorry to disappoint, but there's no puppet master.

"So, if raw chart patterns don't explain much, it has to be the news." One would think so, but as I've explained in the past, news events, also known as "fundamental analysis", are typically supplied after the bitcoin price has already begun moving in a particular direction. Why did the price fall in May-July? "Because China. And Elon." Why did it fall last Monday, September 20th? "Because China." The newest China ban was announced on September 3rd but somehow only began to filter to Western media outlets on Sept 20th. Indeed, fundamental analysis, particularly with Bitcoin, is always supplied after a move has occurred or is occurring. And because Bitcoin "insiders" cannot actually exist insofar as there is no centralized entity to be "inside of", no one has the ability to front-run (aka insider trade) the news cycle. (I suppose "whales" are the Bitcoin version of "insiders".) And even if someone did have the ability to front-run a press release, one single holder no longer has the power to move the market in a significant manner. In the past, when Bitcoin had the market cap of many of the present-day shitcoins and global adoption was under 1%, the market was far more responsive to fundamental news events, but today that appears less and less the case. News events don't even influence many of the alts as they once had. El Salvador's adoption of Bitcoin as legal tender, given the magnitude of the event - something that would have been unheard of 12 months ago - "should" have shot the price to the moon, while Twitter's announcement of their "tipping feature" which opens its 206 million users to the Bitcoin Lightning Network, a global, frictionless, monetary payment matrix, should have propelled Bitcoin beyond the moon to Mars. In the case of El Salvador and Twitter, Bitcoin the "monetary network" is actually allowing millions of individuals to "buy coffee" and carry out immediately settled microtransactions virtually cost-free using not Bitcoin but their traditional bank account(s) to pay mortgages, taxes, debts, and daily necessities. Soon it will be billions of people. The implications of both these events are absolutely monumental, but they hardly had any positive impact on the price. Bitcoin crashed the day El Salvador ratified the legal tender law. Maybe the market hasn't "digest it" yet. Ha ha. So, negative news, even when supplied after the fact, has a greater negative impact on the Bitcoin price while positive - even earth-shattering news - barely moves the needle, what gives?

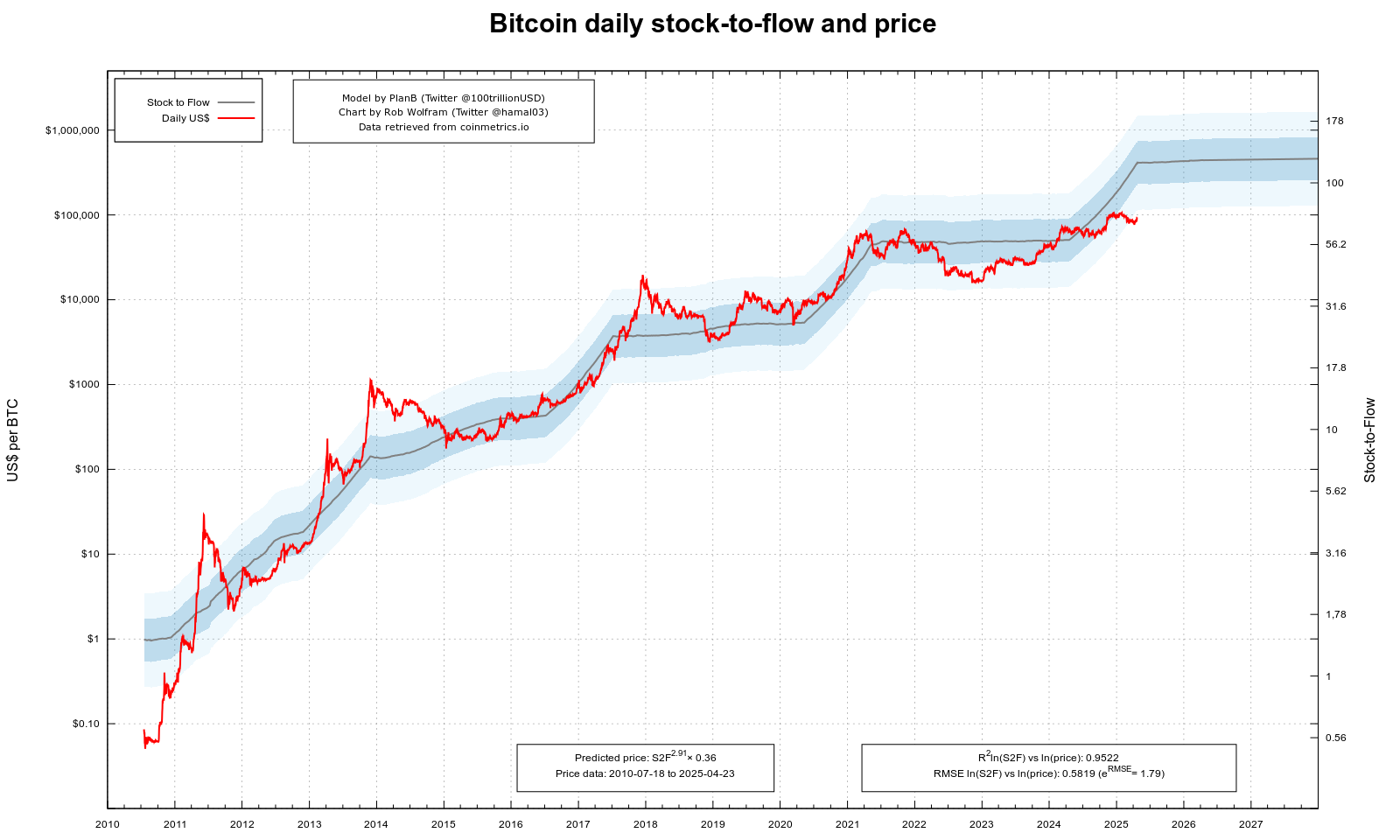

Plan B discusses this quandary in an article entitled, "The Efficient Market Hypothesis and Bitcoin Stock-to-Flow Model." Efficient Market Hypothesis (EMH for short), proposed by the Austrian economist Friedrich Hayek, states that "markets are highly efficient information processing systems, delivering the best possible real-time price discovery". An "efficient market" is one that has already "priced in" certain known and unknown future variables in the present price. Markets can be "weakly efficient", "semi-strong", or "strong". Weakly efficient markets already have historical price data factored into the current price but are responsive to news events and insider information; "technical analysis and time series analysis do not [give one a trading edge]" in weakly efficient markets. Semi-strong markets already have historical price data and fundamental analysis priced in, meaning they will be unresponsive to news events in real-time but are subject to insider information; for semi-strong markets, fundamental analysis does not provide a trading advantage. Strongly efficient markets are those that have virtually every conceivable factor already priced in; not even insider knowledge gives one an edge. Of note, most economists agree that the majority of markets are either weakly efficient or semi-strong. Strongly efficient markets are rare. Bitcoin, according to my observations above, appears, on the one hand, to be semi-strong efficient (i.e. unresponsive to most fundamental analysis), but at the same time slightly less than weakly efficient, insofar as two of its main inflation attributes are widely known but obviously not priced-in to the current Bitcoin valuation: i. e. its hard-capped supply of 21 million coins (which will be mined until the year 2140) and its fixed supply issuance which gets cut in half every four years (aka "The Bitcoin Halving"). If Bitcoin was "weakly efficient", according to Hayek's definition, the Bitcoin price would reflect these attributes and it would be substantially higher than it is currently; the market would also not experience the 4-year halving cycle manias and "crypto winters". Because it does experience these things means that something else is afoot with this asset.

Diving deeper, an investor can assume EMH to be correct and yet still turn a profit if one is willing to take on risk, in other words, "the potential for loss". This is obvious. What is not so obvious is that Bitcoin's current price should be far higher based upon its historic level of risk/volatility compared to its realized reward. Bitcoin has historically achieved a 200% annual return compared to an 80% risk of loss. In a bear market, one can easily expect bitcoin to drop by 85% (95% for most altcoins). For perspective, bonds have an 8% risk but only a 6% return, gold 33% risk, 7.5% return, stocks 40% risk, 8% return. Bitcoin's risk-to-reward, being highly positive, is completely off the charts and therefore difficult to compare to traditional assets. At first glance, one would look at Bitcoin's risk/reward and think the calculations were wrong, that it's a scam, or not an investible asset at all, at least not one we're accustomed to. Because of its "off the charts" risk/reward ratio, Bitcoin should, in my opinion, sit on the balance sheets of virtually every company, hedge fund, and pension fund in the world, but of course, it's not. Why?

The only explanation is that the threat of the unknown that Bitcoin and only Bitcoin among the entire crypto ecosystem introduces is so terrifying and fraught with uncertainty that investors, from big to small, are justifiably unable to envision a world in which Bitcoin actually succeeds because it looks drastically different than the present. Ever since Bitcoin definitively intruded into the world's awareness in 2017 - because the price has consistently underperformed its risk/return ratio from that time forward - the market has, aside from a few small peaks, been overestimating Bitcoin's risk in the long term, and underestimating its potentiality in the near term. Hence a country has christened it legal tender and the price falls. It's usually the opposite for technological adoption cycles wherein most investors overestimate the technological breakthrough in the short term, and underestimate long-term potentiality, the best example being Amazon. This investor sentiment appeared to hold true for bitcoin before 2017 when it was small and unthreatening but since then, that has not been the case. Most shitcoins are enjoying this "near term overestimation, long term underestimation" phenomenon but that is probably due to their immature life cycles and low market caps. Curiously, shitcoiners can somehow see their pet projects surviving while Bitcoin fails. This, I think, is the height of ignorance. If bitcoin fails, they all fail. If state-level actors, which I believe are the only legitimate threats, can kill Bitcoin (principally through overregulation), they can undoubtedly kill any altcoin on the market because none are decentralized and all enjoy the happy shade provided by Bitcoin's mighty shield -- a shield that must remain a bulwark against authoritarian overreach or, as stated, no more "crypto". Bitcoin can, however, quite easily survive while the rest of "crypto" fails. Though I personally don't want this to happen and feel strongly that crypto should be allowed to innovate and disrupt without undue oversight and regulation, it's likely this won't be the eventual outcome, at least in developed countries.

The following is a list of risks commonly espoused by would-be investors over the years:

{kind=link}

Risk that bitcoin dies

Risk of fatal software bugs

Risk of exchange hacks

Risk of 51% attacks by centralized miners

Risk of miner death spiral after halving

Risk of hard forks

Risk of extreme overregulation

Risk of governments making bitcoin illegal

Risk of bitcoin being subsumed by the altcoin market, lagging development, lack of interest

I've covered most of these in past newsletters, but I think the two biggest risks that the market is overestimating are the "risk of governments making bitcoin illegal" and the "risk of bitcoin being subsumed by the altcoin market, lagging development, lack of interest". Institutions are principally concerned with the former while retail the latter. These are, indeed, justifiable risks that all investors must consider as central to their crypto education, but in "placing the correct bet", one could potentially realize not only life-changing wealth but a sense of financial security amid economic turmoil, and also provision for your future generations. Moreover, these risks are not exclusive to Bitcoin, virtually every coin that endeavors to achieve the standing of BTC will have to face these threats and prevail. While I believe only Bitcoin is uniquely designed and has organically developed to overcome these risks, particularly government-level attacks, it is not a foregone conclusion that Ethereum or, say, Cardano might not also be able to develop their own anti-fragility, but this can only be realized over a long, hostile time period. They also have their own unique risks that Bitcoin does not (smart contracts bugs, visible founders/leaders, et al).

Overestimating the risks to Bitcoin while at the same time underestimating the same risks with regards to altcoins (and ignoring the unique risks of each particular project) proves to me as a seasoned market participant that crypto investors are wrongly interpreting the available market data and therefore sending miscalculated, skewed price signals. This likely explains the overvaluation of virtually everything besides Bitcoin and Ethereum and the undervaluation of the top two projects. Only Ethereum has consistently proved itself capable of maintaining its #2 position since it attained it, while the rest of the top 10, to say nothing of the remaining top 20, has shifted like a shuffled deck of cards year after year. Here is a snapshot of the top 10 coins at the peak of the market frenzy in 2017.

XRP and Cardano have remained, but the others are much further down the market cap list. History will rhyme this cycle as well, of that there can be no doubt.

Perhaps the reason the market is sending what I believe to be the wrong signals is due to the fact that crypto is open, global, accessible, easy to use, unregulated, and made available to retail money before institutional investors; retail money who, as a collective body, are generally less researched, less experienced, and more easily swayed by hyperbole as compared to accredited investors who are not so easily swayed. This, combined with the general ignorance of this technology and the lack of "grand vision" as to what the future might hold has perhaps baked into the crypto market false signals that are more responsive to clever marketing than underlying fundamentals and actual working products. Whether true or not, only time will tell.

I've often asked myself how an entire market composed up of many diverse participants, when presented with the clear technological advantages of bitcoin over the other projects (not only in terms of "digital money" and "digital store of value" but as something akin to an internet-like protocol layer similar to the internet's own TCP IP), in light of the above-mentioned risks and also our present macroeconomic and geopolitical environment, can collectively "miss this"? Maybe it's fear. Or maybe it is humanity's inevitable plight to mistake the actual revolution playing out before them in plain sight with that which is "full of sound and fury, signifying nothing".

Good luck to you all.